Central Bank Digital Currency (CBDC)

A new form of digital money.

According to the International Monetary Fund (IMF), the Central Bank Digital Currency (CBDC) is a new form of digital money, issued by a central bank and is intended to be legal tender. Economically, the CBDC is backed by legislation to be equivalent in value to the respective fiat currency and is fully backed and regulated by the respective central bank.

CBDCs are an interesting evolution of money whereby blockchain technology and smart contracts are utilised to reduce transaction cost and payment friction associated with cash with the eventual goal of providing equal access to payment, thereby improving financial inclusion. The blockchain technology will also allow central banks and governments alike to finetune monetary policy changes more effectively as well as carry out more targeted fiscal transfers.

The idea of CBDC is not new. There have been attempts by central banks to introduce CBDCs since the 1990s but in quite different forms. For example, Bank of Finland’s Avant system in 1992 and Ecuador’s Sistema de Dinero Electrónico in 2014; however, both were short-lived.

More recently in 2020, Sweden's Riksbank noted the consequences and potential problems arising from the “marginalisation of cash” as cash usage dropped to a low of 7% of total transactions. As a result, the Riksbank initiated a pilot project to develop a technical solution for the Swedish Krona in digital form, i.e. a CBDC version in the form of a e-Krona.

Closer to home, Cambodia launched its domestic version of a retail CBDC in 2020. Called the Bakong, it is meant to improve financial inclusion and allow citizens to perform basic transactions on their smartphones.

With the emergence of new technologies such as blockchain or distributed ledger technologies (DLT) and rise of stablecoins, there has been overwhelming interest in CBDC over the last 18 months. As stablecoins become popular, central banks may be looking to provide alternatives, such as a new form of central bank money.

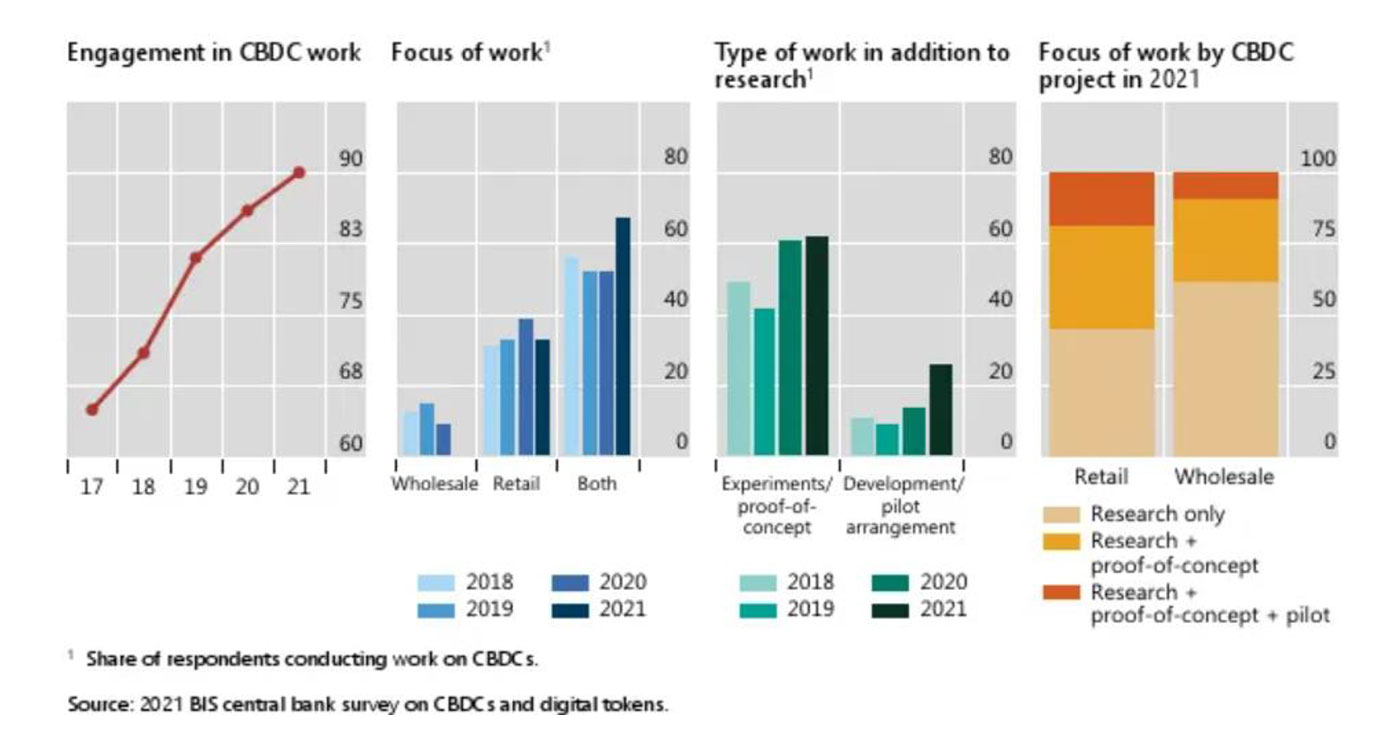

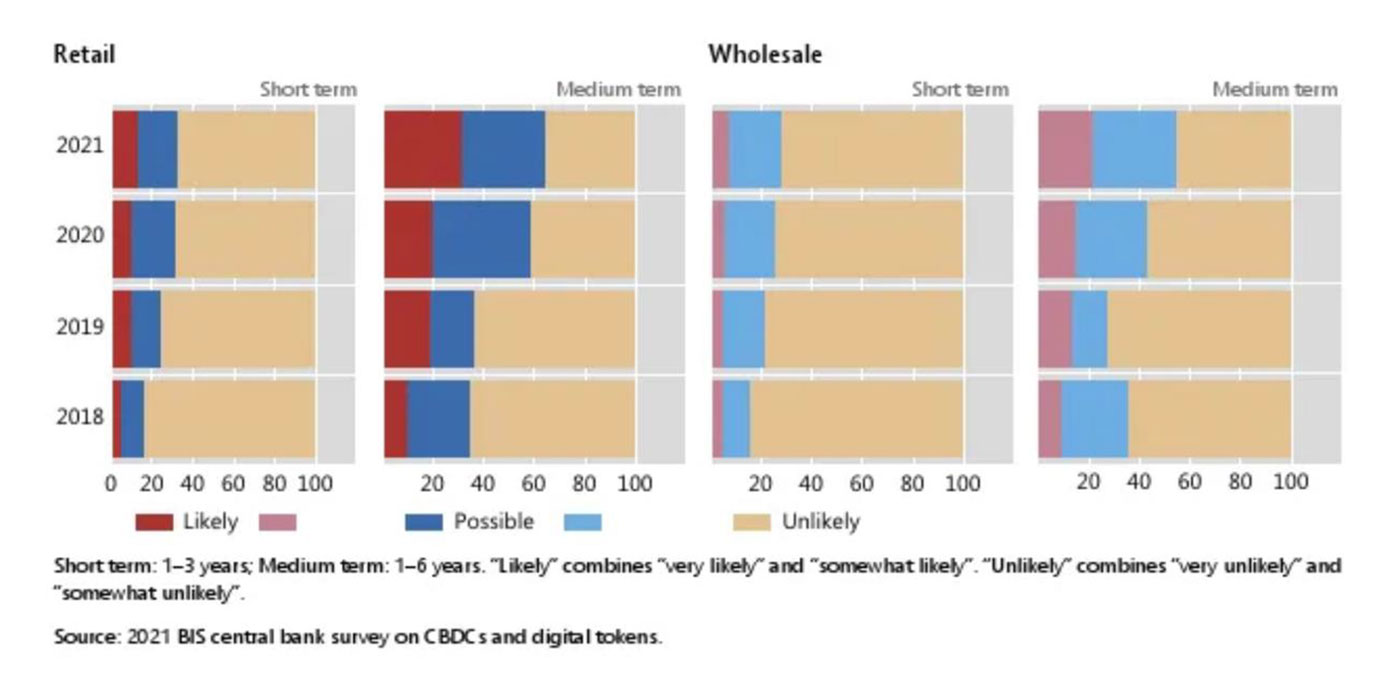

According to the latest Bank of International Settlements (BIS) survey on CBDCs published in May 2022 (Paper No. 125), the BIS noted that nine out of 10 central banks are exploring CBDCs in one form or another and that more than half are now developing them or running concrete experiments. The BIS survey also noted concrete examples of successful CBDC rollouts, e.g. The Bahamas has launched their version of retail CBDC, called The Sand Dollar in 2020 and China continues to expand its domestic pilots for the e-CNY. The BIS survey interviewed 81 global central banks and noted that a record share of 90% of those surveyed is engaged in some form of CBDC.

Over the past two years, many Asian central banks have embarked on their respective domestic studies of CBDCs. The People’s Bank of China (PBoC) has led the race with extended domestic public trials and pilots of the e-CNY. There have also been various collaborative studies on CBDCs as well. In 2017, the Hong Kong Monetary Authority (HKMA) collaborated with Bank of Thailand (BoT) on a joint wholesale CBDC study for cross border payment under the auspices of Project Inthanon-Lion Rock.

Most recently in Sep 2020, the BIS announced that it had successfully conducted trials under its m-Bridge CBDC pilot. The m-Bridge is an international CBDC study involving the Hong Kong Monetary Authority (HKMA), BoT, PBoC and Central Bank of the UAE. Altogether, 20 participating banks conducted over 160 transfers and FX trades, worth a total of over USD 22 million, focusing on cross border trade.

While there is no compelling case for retail CBDC in Singapore given well-functioning payment systems and broad financial inclusion, infrastructure and technical competencies are being developed domestically through Project Orchid. As there is good potential for wholesale CBDC, Singapore continues to participate in cross border CBDC projects such as Project Dunbar to explore common multi-CBDC platforms to enable cheaper, faster and safer cross-border payments. UOB participates in both Project Orchid and Project Dunbar.

China is at the forefront of the CBDC race. Domestically, CBDCs have been piloted in over 23 cities, with highly incentivized adoptions achieving more than a hundred million individual users and billions of yuan in transactions. On the cross-border front, China is entering phase 2 technical testing of cross-boundary use of e-CNY with Hong Kong and is actively participating in mCBDC Bridge test for real-time, cheaper and safer cross-border payments and settlements.

Hong Kong is working on laying the technological and legal foundation for CBDCs while delving into use cases, applications as well as implementation and design issues. It is conducting pilot tests where all the learnings would feed into the onward implementation planning and timeline for launching e-HKD.

Thailand is piloting retail CBDC with approximately 10,000 retail users between end-2022 and mid-2023 to assess the suitability of its technology and design of its CBDC. It is exploring CBDCs for cross border payments with Hong Kong, China and UAE through m-bridge.

Indonesia is researching CBDCs, with plans to issue a whitepaper and release the conceptual design of digital rupiah for banks to use by end-2022.

While Malaysia has no immediate plans to issue retail CBDCs, it has participated in Project Dunbar and has initiated a multi-year CBDC exploration effort.

Vietnam established a working group in 2020 to explore digital assets and digital currencies with the aim to research, develop and pilot CBDC using blockchain technology between 2021 to 2023.

While many open questions remain, some of the key lessons learned thus far includes:

As central banks continue to explore, learn, experiment with and design CBDCs, we should see more public-private sector collaborations and sharing of best practices across countries to further enrich this exciting journey.

Based on central bank interest today, it is likely that CBDCs will be launched in the medium-term. The trend is likely to continue as the future of the retail CBDC ecosystem comes into sharper focus and the potential role of CBDC in improving cross-border payments efficiencies is further explored.

The G20 TechSprint 2022 focuses on solving technology challenges related to wholesale and retail CBDCs. Global innovators are invited to develop new solutions to solve the following three key challenges:

"There is a collective belief that CBDCs have potential for promoting the public interest in this age of digital money. Trust in money is the glue that holds the financial system together. It is for this reason that, as technology advances, central banks must ensure that the monetary system remains fundamentally a public good and preserve its stability."

Agustín Carstens, General Manager of the BIS

UOB views CBDCs as one of the key pillars in blockchain applications that will significantly transform the payment landscape in the years to come. Currently, there are many different types of CBDCs under study, ranging from retail and wholesale CBDCs to cross-border CBDCs as well as Purpose Bound Money (PBM).

To that end, UOB aims to work and collaborate with regional central banks across Asia and ASEAN to help bring central bank-led CBDC innovations to the region and our clients.